These days it's impossible to talk about the real estate market and the economy separately. There are a lot of popular fallacies floating about, and many people use the economic crisis as fodder for their favorite prejudices. Last fall I was reading the newest post on a somewhat high pitched, but content heavy real estate blog, and was taken aback by the comments by posters. One made a racial epithet at Obama, another blamed all our problems on illegal immigrants, and the third declared that it was "a conspiracy of jewish bankers." I'm not making it up.

I recently had a conversation with somebody, and he laid the blame for the real estate crash and consequent economic troubles squarely on "minority lending." I can't say I was surprised. Our short attention span "news" media encourages simplistic answers and those pesky "minorities" - and poor people in general - serve as popular escape goats.

This same person also told me that it was all the fault and Fannie Mae and Freddie mac, and that the government "forced banks" to make those sub-prime loans. He also opined that the crisis was "limited to the finance sector" and that the economy wasn't all that bad all will be well within a few months.

I'm not an economist, or an expert in any way, but I've made a concentrated effort to understand what is going on behind the curtain. My motivation is simple: I hope to be a home owner one day, and hope to do it without the mistakes others made. Also I'm simply curious. I believe these are historically interesting times. I hoped never to live in such times, but might as well appreciate them.

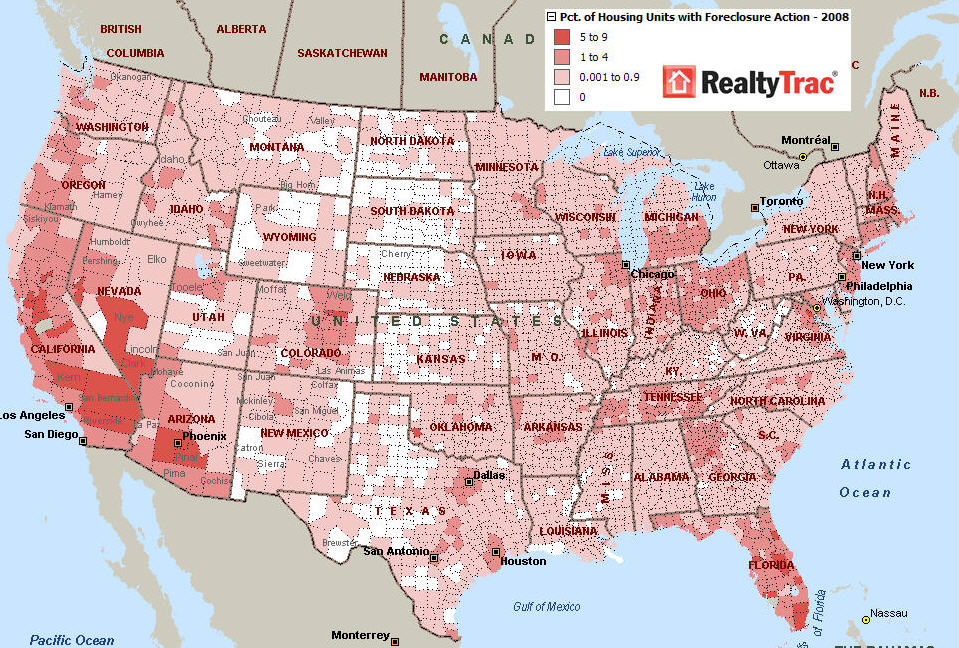

The first fallacy about the real estate bubble that it is all about the sub-prime loans. In the next two years we will learn how false this is, as we hear more and more about the Option ARM and Alt-A mess. Another huge wave of foreclosures is heading our way, this time putting the crunch on the higher end of the market. (I suggest following West Side Bubble blog if you are interested in this segment of the market.)

The Option ARM and Alt-A loan calamity will void the "those greedy minorities caused this mess" myth. Dr. Housing Bubble had a very informative post about how toxic these loans are. They were given to borrowers with good credit, and generally for far larger amounts than the sub-prime loans.

Second fallacy is that it's all because of Fannie Mae and Freddie Mac. While no doubt these companies are problematic, they actually played a small role, especially compared to other financial institutions involved. An excellent article by Paul Krugman explains Fannie and Freddie in detail.

So how did this whole mess came about? It's a little bit complicated. It all started with deregulations that enabled financial institutions, Wall Street to engage in much riskier practices than before. Banks and mortgage companies begin to look for ways of making more money, so they relaxed their lending standards. This NYT article about how it happened at WaMu is an example of an industry-wide exuberant insanity and irresponsibility. From CEOs to loan officers, to appraisers got paid big bonuses for chasing the short term profit that ended up bankrupting companies. Countrywide's ad is pure comedy if you look at it now, but at the time it was serious. Real estate agents deserve a nod too. Their interest dictated that the more expensive the house was the better, and didn't care where the money came from.

The next big player was Wall Street as they bought the toxic loans from banks and sliced and diced them repackaged them and sold them off. Another NYT article helps to get a better grasp of this complicated mess that we laymen have a hard time understanding. Credit Default Swaps and leveraging feature prominently.

The biggest fallacy of all is "Housing Prices Never Go Down." Along with its little brother, "real estate is the best investment" this fallacy fooled a lot of people into taking unreasonable risks. Those two were basically used to clobber common sense. In reality, normally nominal housing prices keep going up only because of inflation. Inflation adjusted housing prices zig-zag around a base line, and are just as likely to go down as up. Overall real estate is only good investment if you catch a bubble and sell before it pops. It's riskier than playing the stock market. And well, apparently housing prices do go down.

But there is more. There is a deep ideological reason why this cascade of egregious mistakes and bad decisions was allowed to happen. Big Picture has a wonderfully lucid piece - a comment and critique on yet another NYT article - by Bailout Nation author Barry Ritholtz about the most fundamental reason that led us to the current financial crisis:

"...these decisions were driven not by pragmatic realism, not bad attempts at problem solving, but rather, due to an intellectual free market jihad. They were caused by a radical deregulatory zeal that could only be affected by “religious” ideologues."